Section 87A of the Income Tax Act, 1961 provides a tax rebate to resident individual taxpayers whose total income does not exceed a specified threshold. For the financial year 2023-24 (assessment year 2024-25), under the new tax regime, individuals with a total income up to ₹7,00,000 are eligible to claim a rebate of up to ₹25,000. This effectively means that no income tax is payable if the income is within this limit. However, if the income exceeds ₹7,00,000 even by a small amount, the rebate is not available, and the entire tax becomes payable there is no marginal relief under the new regime. This provision is aimed at reducing the tax burden on low and middle-income earners and encouraging taxpayers to opt for the simplified new tax regime.

Facts of the case:

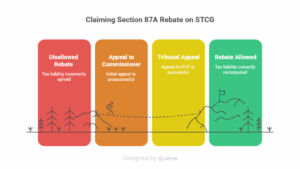

- The assessee, an individual resident of India, had originally filed her return of income under section 139(1), declaring total income of Rs.4,27,635, comprising short-term capital gains under section 111A, long-term capital gains under section 112A and income from other sources. The return was subsequently revised to correct certain omissions in the capital gain schedule. In the revised return, the assessee exercised the option under section 115BAC(1A), e.,to be governed by the default new tax regime applicable from assessment year 2024-25 as amended by the Finance Act, 2023. The total tax liability computed under the revised return amounted to Rs. 13,320, arising solely on account of STCG under section 111A, which was chargeable at 15 per cent.

- The assessee being a resident individual with total income below Rs. 7,00,000, claimed rebate of Rs. 13,320 under section 87A, as per the first proviso to section 87A inserted by the Finance Act, 2023, which allows a rebate up to Rs.25,000 to an individual whose income is chargeable under section 115BAC(1A), provided the total income does not exceed the threshold. The return was processed by the Centralised Processing Centre (CPC), Bengaluru, and intimation under section 143(1) was issued, whereby the assessee’s claim of rebate under section 87A was disallowed. The tax liability of Rs. 13,319 was upheld, and together with interest under sections 234B and 234C and health and education cess, a total demand of Rs. 15,820 was raised.

- On appeal, the Commissioner (Appeals) acknowledged that the first proviso to section 87A permits rebate for individuals whose total income is chargeable under section 115BAC(1A), but clarified that such computation is expressly made subject to the provisions of Chapter XII, which includes special rate incomes such as STCG under section 111A and LTCG under section 112/112A. Therefore, tax on such special incomes cannot be offset or reduced by the rebate under section 87A, even under the new regime.

- On appeal to the tribunal:

- The appeal of the assessee was allowed

Conclusion

It was held that, in the appeal for Assessment Year 2024‑25, the ITAT Ahmedabad (SMC Bench) held that a resident individual, who opted for the new tax regime (Section 115BAC(1A)) and whose total income did not exceed ₹7 lakh, was entitled to claim the Section 87A rebate even when her tax liability arose solely from short‑term capital gains (STCG) taxable under Section 111A. The Tribunal emphasized that neither Section 87A nor Section 111A contains any express bar on granting the rebate in such circumstances, unlike Section 112A(6), which explicitly restricts rebates on LTCG. The inclusion of “special rate” incomes under Chapter XII for computation purposes does not override the operation of Section 87A, which functions independently and after tax is computed. The Tribunal also dismissed reliance on the explanatory memorandum to the Finance Bill, 2025 highlighting that it cannot alter the unambiguous text of the prevailing law.

As a result, the ITAT allowed the rebate of ₹13,320, directed the Assessing Officer to recompute the tax liability accordingly, and deleted the demand of ₹15,820 raised by the CPC.

Land not used for any agricultural purpose couldn’t be treated as agricultural land; SLP dismissed

Section 2(14) of the Income-tax Act, 1961 – Capital gains – Capital asset (Agricultural land) – Assessment year 2011-12 – Assessee sold a plot of land and claimed that it was an agricultural land and, thus, not a capital asset – Assessing Officer, Commissioner (Appeals) and Tribunal recorded concurrent findings of facts that land in question was not used for any agricultural purpose and therefore, income derived from sale of such land was chargeable to tax – It was noted that authorities had considered all evidence, including self-serving ledger entries and revenue records – Authorities had also considered conveyance by which assessee, after developing this property into plots, sold same to other parties – Authorities also considered contradictory stances of assessee and its proximity to developed areas inferring that this property was embedded with commercial opportunity and viability for commercial exploitation – All findings of fact were supported by more than adequate material on record and no legal principle concerning appreciation of evidence had been violated – High Court by impugned order held that, there being no reasonable grounds to interfere with finding of fact recorded by three authorities concurrently, appeal was to be dismissed – Whether instant court was not inclined to interfere with impugned judgment/order of High Court – Held, yes – Special Leave Petition filed by assessee was to be dismissed – Held, yes [Para 1] [In favour of revenue]

Loss on trading in derivatives is business loss and not speculation loss; can be set off against business income: HC

Section 43(5) of the Income-tax Act, 1961 defines a speculative transaction as one where a contract for the purchase or sale of commodities or shares is settled without actual delivery. However, certain transactions like hedging contracts, and trading in derivatives or commodities on recognized stock exchanges are specifically excluded and not treated as speculative.

Read with Section 73, the Act imposes restrictions on the treatment of losses from speculative business. Such losses can only be set off against speculative profits and may be carried forward for four years. Additionally, Section 73 deems that companies primarily engaged in share trading are carrying on a speculative business, even if the transactions involve actual delivery. Thus, while a transaction may not be speculative under Section 43(5), it can still be treated as speculative under Section 73 for tax purposes, especially in the case of companies

Facts of the case:

- The assessee was engaged in the business of trading of derivatives, e.,future and option transactions including trading in goods and merchandise. During relevant year, the assessee had incurred losses from trading in derivatives and claimed set off of the same against profits of the business.

- The Assessing Officer invoked the Explanation to section 73 treated the loss in question as speculative loss. He, thus, disallowed the claim of the assessee.

- On appeal, the Commissioner (Appeals) held that losses incurred from trading in derivatives were business losses under the proviso to section 43(5) and not speculation losses. He, thus, allowed the claim of the assessee.

- On appeal, the Tribunal held that the future and option transactions were not covered by Explanation to section 73, thus, loss on trading of futures and options could be set off against business income.

- On appeal to high court:

- The substantial question of law raised by the revenue in the instant case was considered by the Division Bench of this court in the case of Asian Financial Services Ltd. v. CIT[2016] 70 taxmann.com 9/240 Taxman 192 (Calcutta). In the said appeal filed by the assessee identical question of law was raised in the said reported decision. The Division Bench allowed the assessee’s appeal.

- Applying the law laid in the above decision, it is to be held that the loss incurred on account of derivatives would be deemed to be business loss under the proviso to section 43(5) and not speculation loss and, hence, Explanation to Section 73 could not be applied; as such, loss would be set off against income from business.

- Thus, the appeal filed by the revenue is dismissed and the substantial question of law is answered against the revenue.

Exp. incurred on ESOP & ISOP to be allowed as deduction if same was duly incurred & fully substantiated: ITAT

Section 37(1) of the Income-tax Act allows a deduction for any business expenditure that is wholly and exclusively incurred for the purpose of the business or profession but is not specifically covered under any other section of the Act. This section acts as a residual provision to permit deduction of legitimate business expenses that do not fall under specific heads like salaries, repairs, or depreciation.

The key conditions are that the expenditure must be incurred during the course of business, be revenue in nature, and not be capital, personal, or illegal expenses. Common examples include payments for legal fees, professional charges, and other general business expenses.

Facts of the case:

- The holding company (US company) of assessee company had formulated and administered globally integrated stock-based compensation schemes, namely the Employee Stock Option Plan (ESOP) and the International Stock Ownership Plan (ISOP), which were extended to the employees of the assessee-company. Under the ESOP scheme, certain eligible employees of the assessee were granted rights to receive stock-linked benefits upon fulfilment of prescribed vesting conditions. The assessee bore the cost proportionate to the employee’s service rendered in India.

- The assessee claimed expenditure paid to the holding company towards ESOP and ISOP.

- The Assessing Officer disallowed the entire claim on the ground that the expenditure did not crystallise during the relevant previous year and was in the nature of contingent or notional outlay, lacking actual cash outflow or irrevocable obligation.

- The Commissioner (Appeals) affirmed the disallowance made by the Assessing Officer.

- On appeal to the Tribunal : The assessee submitted that it merely reimbursed the holding company for that portion of benefit attributable to Indian employees, based on vesting or contribution criteria, and the corresponding payments were actually made, tax deducted, and recorded in the books.

Conclusion

- The disallowance made by the lower authorities does not stand the test of law or fact.

- The ESOP and ISOP schemes originate from the foreign holding company and involve no issuance of shares or premium by the assessee. The assessee merely reimburses actual costs in relation to its own employees, which are recorded in the books and supported by actual payments and TDS deduction.

- The evidences produced cross-charge invoices, foreign remittance documentation, and perquisite reporting clearly establish the crystallisation of liability and actual outgo in the relevant previous year.

- The argument that the expenditure is capital in nature due to linkage with shares is misconceived. The shares are those of the holding company, not the assessee. No capital advantage accrues to the assessee, nor is there any change in its capital structure.

- Moreover, the principle of commercial expediency mandates allowance of any expenditure incurred to secure competent workforce and ensure organisational growth.

- In the instant case, the assessee’s outlay towards ESOP and ISOP represents a conscious, business-driven compensation mechanism to reward and retain employees. The cost is real, the benefit is quantifiable, and the purpose is unambiguously business-centric.

- In view of the foregoing analysis, the disallowance made under section 37(1) is unsustainable. The expenses are duly incurred, fully substantiated, and allowable as revenue expenditure.

Also Read : Income Tax Department cracks down on bogus claims of Deductions & Exemptions