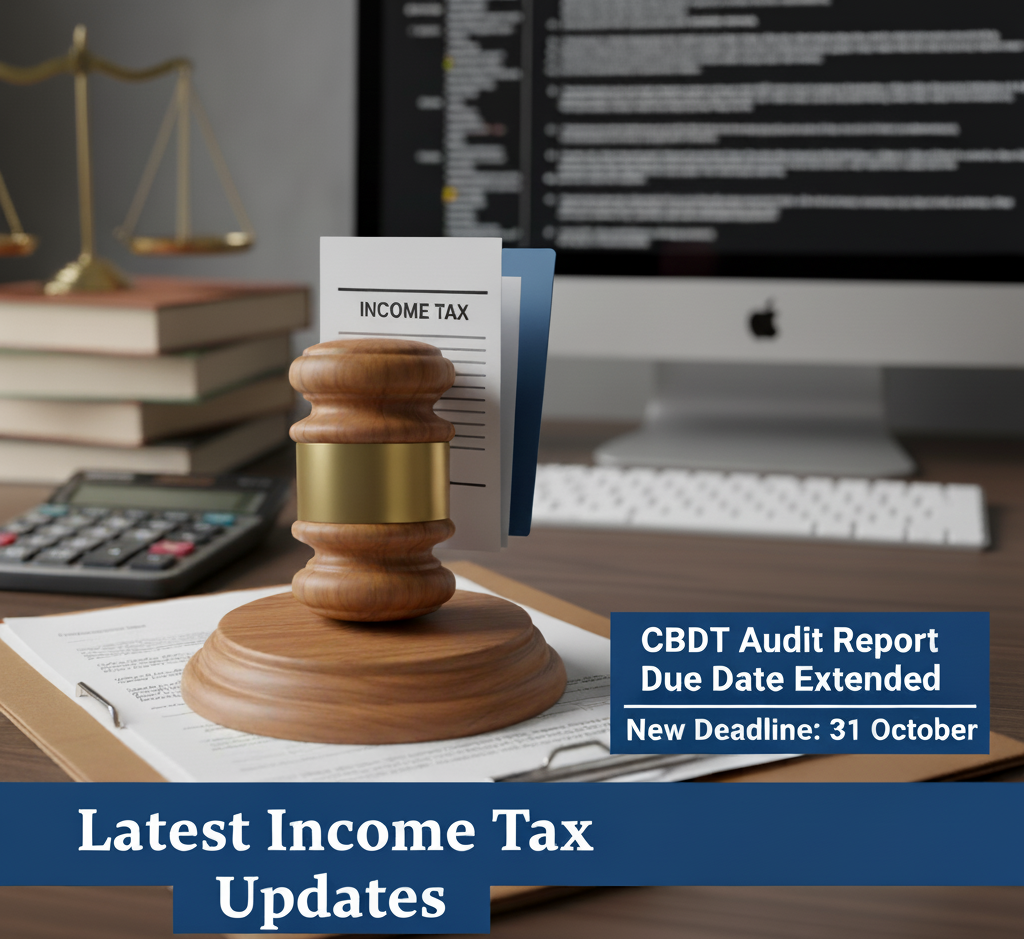

CBDT extends due date for filing Tax Audit Report for A.Y 2025-26 to 31st October 2025

The Central Board of Direct Taxes (CBDT) has extended the due date for furnishing audit reports under the Income-tax Act, 1961 for AY 2025-26 (PY 2024-25).

· Original Due Date: 30th September 2025

· Extended Due Date: 31st October 2025

This relief follows representations from professional bodies citing hardships faced by taxpayers due to natural calamities and disruptions in professional activities. The extension has been granted considering practical difficulties and submissions before Honourable Courts.

**************

Deduction u/s 54F allowed as assessee utilized sale proceeds for constructing house.

Section 54F provides capital gains exemption when an individual or HUF sells any long-term capital asset (other than a residential house property) and invests the net sale consideration in purchasing or constructing a residential house.

Facts of the case:

1. The assessee sold gifted immovable property, received Rs.69 lakhs and invested sale proceeds in construction of a new house. The assessee claimed deduction under section 54F.

2. The Assessing Officer noted that as per the compensation paid by the Government for compulsory acquisition as in which land sold by assessee was situated. The compensation of Rs.3.50 lakhs per acre was declared on 6-8-2006. The claim that he had filed plea for enhanced compensation and hence higher value be taken. So market value was considered as per settled value rather than adhoc value. So full value of FMV as on 1-4-2001 was Rs.9.89 lakhs. He further noted that the property was sold on 25-1-2018 for claim of deduction under section 54F in the financial year 2017-18, the amount should have been kept in the capital gain account claimed by the assessee by the due date of filing of ITR. However, the assessee had not deposited the proceeds from transfer of capital asset in

capital gain account scheme account. Hence, the amount spent on construction of house in financial year 2018-19 starting from January 2019 was not allowed under section 54F.

3. The Assessing Officer allowed index cost of acquisition of Rs.26.92 lakhs and deduction under section 54B was allowed of Rs.16.01 lakhs. Accordingly, long term capital gain was calculated at Rs.26.06 lakhs.

4. On appeal, the Commissioner (Appeals) observed that the assessee did not satisfy the condition of section 54F(2) and 54F(4) and he dismissed the appeal of the assessee.

5. On appeal to tribunal:

i. ) It was held that During the course of assessment proceedings, assessee has furnished documents in support of expenditure incurred towards construction of house but the Assessing Officer has not made any comment on the same. He observed that the assessee has not deposited the amount in CGAS the amount is not utilized within the due date of filing of return of income under section 139. The assessee has been allowed under section 54B. The amount was kept in the nationalized bank and the assessee withdrew amount from the bank and incurred expenditure towards construction of the house property.

**************

Application seeking regular registration under section 80G(5) filed 6 months before expiry of provisional approval valid and maintainable: ITAT

Section 80G of the Income-tax Act, 1961 provides tax deductions to encourage donations made to certain funds, charitable institutions, and approved organizations. Any taxpayer—individual, HUF, firm, or company—can claim deduction under this section, provided the donation is made in monetary form (cash up to ₹2,000, or through cheque, draft, or electronic transfer for higher amounts). The recipient institution must be approved under section 80G(5), and a valid receipt mentioning its name, PAN, address, registration number, and donation details is required. The deduction allowed depends on the nature of the fund or institution: in some cases, it is 100% of the donated amount without any limit, while in others, it may be 50% or 100% of the donation subject to a cap of 10% of the adjusted gross total income. Prominent examples include 100% deduction without limit for donations to the Prime Minister’s National Relief Fund, PM CARES Fund, or the National Defence Fund, while donations to other approved charitable trusts are generally eligible for 50% deduction subject to the 10% income ceiling. Thus, Section 80G serves as both a social incentive for taxpayers to contribute to public welfare causes and a financial relief by reducing their taxable income.

Facts of the case:

1. The assessee by filing an application in Form 10AB on dated 30-9-2024 under clause (iii) of 1st Proviso to section 80G(5) had sought for approval under section 80G on the ground that the assessee had obtained provisional approval under section 80G vide order dated 4-10-2022 valid from 4-10-2022 to assessment year 2025-26.

2. The Commissioner (Exemptions) rejected the application filed by the assessee by holding the application was belated as not filed within six months of the commencement of the activities, as prescribed in the provisions of section 80G(5).

3. On appeal to tribunal:

Held:

1. From the provisions of section 80G(5), it appears that there are two conditions and/or two time limits for seeking regular registration under section 80G(5), such as application should have been filed at least six months prior to expiry of the period of provisional approval or within six months of commencement of its activities whichever is earlier.

2. In the instant case, the assessee has claimed and not denied by the revenue that the assessee was established in 1952 and registered/certified as institution/fund established in the taxable territories for charitable purposes, vide certificate dated 23-9-1975 by the Commissioner and since then has been enjoying exemption under section 11 and the benefit of the section 80G. However, pursuant to the Amendment vide Finance Act, 2022, the assessee had applied and got provisional approval under section 80G(5) on dated 4-10-2022 which is valid up to assessment year 2025-26.

3. As the assessee established in 1952 and commenced its activities in 1952, therefore the 2nd clause for filing an application for regular registration such as, the application is required to be filed within six months of commencement of activities, has no applicability at all to the case of the assessee.

4. As first clause of such provision mandates that the application is required to be filed six months prior to the expiry of the period of provisional approval and thus the assessee has duly filed its application within the time, as prescribed in the relevant clause of the provision of the Act on dated 30-9-2024, as the provisional registration of the assessee is available up to assessment year 2025-26.

5. Thus, on the aforesaid analyzations and applicable provisions of law, the rejection of regular registration sought for by the assessee, vide impugned order by the Commissioner, is unsustainable in the eyes of law.

6. Thus, on the aforesaid analyzations, the impugned order is set aside and consequently the Commissioner is directed to consider the application filed by the assessee as valid and being filed within the limitation period and to decide the same on merit accordingly.

7. In the result, the assessee’s appeal is allowed for statistical purpose.

*************

Income from sale of seeds produced by getting them cultivated through farmers is agricultural income: HC

Section 10(1) of the Income-tax Act, 1961 provides an exemption for income derived from agricultural activities carried out in India. This means that agricultural income, as defined under Section 2(1A), does not form part of the total taxable income of an assessee. Section 2(1A) defines agricultural income to include: (i) rent or revenue derived from land situated in India and used for agricultural purposes, (ii) income derived from such land by agricultural operations, including processing of agricultural produce to make it fit for sale in the market, and (iii) income attributable to a farmhouse subject to prescribed conditions. However, certain related activities, such as income from nurseries, are also specifically treated as agricultural income. While agricultural income itself is exempt under Section 10(1), it is important to note that for individuals and HUFs, such income is considered for rate purposes through the mechanism of partial integration, where agricultural income is aggregated with non-agricultural income to compute the applicable tax slab rate, provided non-agricultural income exceeds the basic exemption limit. Thus, Section 10(1) read with Section 2(1A) ensures that genuine agricultural earnings remain outside the scope of tax, while simultaneously preventing misuse by linking it with other income for determining the correct rate of taxation.

Facts of the case:

1. The assessee–seed company was engaged in research, production and sale of agricultural/hybrid seeds. For AY 2011-12, it claimed exemption of about Rs. 39.26 crores under Section 10(1). The assessee had entered into agreements with farmers to utilize their lands, under which the farmers performed normal agronomic practices (irrigation, fertilization, pest/disease control, weeding, harvesting, threshing) for production of seeds from foundation seeds supplied by the assessee under its supervision and control.

2. The AO issued a notice proposing to disallow the claim under Section 10(1), rejected the assessee’s explanation, and held that the assessee was not directly involved in agricultural activity; production of hybrid seeds

was different from normal crop production, involving elaborate scientific operations and post-harvest physical/chemical treatments; and production on lands owned by farmers, as per the agreements, could not be treated as agricultural operations carried on by the assessee. The AO disallowed the exemption under Section 10(1) and completed the assessment under Section 143(3).

3. On appeal, the Commissioner (Appeals) allowed the assessee’s claim, relying on the Tribunal’s decision in Prabhat Agri-Biotech Ltd., as affirmed by the High Court, and held that operations involved in production of seeds were agricultural and eligible for exemption under Section 10(1).

4. On the revenue’s appeal, the Tribunal followed its coordinate bench decisions, noted that the facts were identical, and held that income generated from cultivation of basic/foundation seeds was agricultural income exempt under Section 10(1), thereby dismissing the department’s ground.

5. On appeal to tribunal:

Held:

1. Admittedly, the assessee herein is a company engaged in the business of research, production and sale of agricultural seeds. The activity which is carried out by the assessee was for the purpose of research and development activity which involves scientific study of the parent seed and hybridization of different varieties of the parent seeds so as to evolve the high yielding of hybrid seeds. The hybrid seeds are generated by certain involved process, which the farmer cannot perform suo motu and that the hybrid seeds are sold in the market different varieties of the parent seeds so as to evolve high yielding variety of hybrid seeds. It is also stated that the assessee would enter into agreements with the farmers for utilization of lands owned by them, wherein the farmer agreed to perform certain agricultural operations including but not limited to normal agronomic practices required for raising a good crop like irrigation, fertilization, pest/disease combat, weeding, harvesting, threshing etc, for the purpose of production of seeds from the said foundation seeds.

2. It is evident from the terms and conditions imposed on the farmers that the farmers raised crops as desired by the assessee and the whole process is in the nature of production through contract.

3. Having considered the judgment of the Hon’ble Supreme Court in CIT v. Raja Benoy Kumar Sahas Roy [1957] 32 ITR 466 (SC) and having considered the entire material placed on record, the parent seeds are produced by way of agriculture and cultivation. As the company gets the cultivation done under its supervision and at its own costs and risks, the production of these seeds, and the farmer wherein under the supervision, technical guidance and control of the company is in agreement for the production of the Hybrid seeds, since they have direct nexus with the land owned by it or on the leased lands by supplying seeds to the farmers and getting them cultivated under its supervision and control and the company plays an active role of action of monitoring and nurturing the plants by the assessee cultivated by the farmers. As there is an element of involvement of assessee by entering into an agreement with the farmers for utilizing the lands owned by them and from such agreements, the assessee company is being utilizing for production of hybrid seeds on mass scale from the foundation seeds on payment of certain compensation. Though the assessee may not be directly involved in the activity of cultivation but it is being involved through farmers for production of hybrid yielding seeds for different types of hybridization and which are used for the purpose of agriculture for deriving high yielding seeds. Therefore, this bench is of the opinion that though the assessee is not directly involved into the agricultural activity, but indirectly they are involved in the said activity.

4. Therefore, for the afore said reasons, this Bench is of the opinion that the Tribunal was justified in allowing deduction under Section 10(1) of the Income-tax Act, 1961 by taking the income of the assessee as an agricultural income and this Bench is of the opinion that there is nothing wrong to interfere with the said finding of the Commissioner of Income Tax (Appeals) and the Tribunal.

Conclusion:

1. In this ruling, the Telangana High Court held in favour of the assessee, Nuziveedu Seeds Ltd, overturning the reassessment made by the revenue authority. The Court found that the Assessing Officer lacked sufficient reason to believe that income had escaped assessment, and the procedural safeguards mandated under the law were not satisfactorily complied with. The decision emphasizes that reopening an assessment under Sections 147/148 requires more than mere suspicion; the AO must point to material evidence or circumstances justifying reassessment. Since the legislative and procedural requirements for reassessment were not met in the case at hand, the High Court quashed the reassessment order.

*************

AO can’t make additions if the assessee didn’t claim deduction of expenses in the ITR: HC

Section 37(1) of the Income-tax Act, 1961, in simple terms, allows a businessperson or professional to claim as a deduction all genuine expenses that are incurred wholly and exclusively for the purpose of running the business, provided such expenses are not capital in nature, not personal, and are not already covered under other specific sections of the Act. This means routine business costs like office rent, staff salaries, travel for business purposes, or advertising expenses are generally deductible. However, expenses that are illegal, prohibited by law, or against public policy—such as bribes, penalties, or fines—cannot be claimed. Similarly, costs that are personal in nature or those used to acquire fixed assets like land or machinery are also excluded. In essence, Section 37(1) acts as a catch-all provision to ensure that all legitimate business expenses are allowed as deductions, while disallowing personal, capital, and unlawful expenses.

Facts of the case:

1. The assessee was a Category II AIF-closed ended fund registered with SEBI. It filed its return declaring nil income. It was an investment fund as defined under section 115UB and earned only short-term capital gains of certain amount which was exempt under section 10(23FBA) read with section 115UB. During year, the assessee implemented investments aggregating to huge amount using the capital raised from its unit holders. The assessee had incurred certain expenses towards management fees and other related costs paid to its investment advisor and other expenses such as personnel cost, salaries, etc. Same were debited to the statement of the profit and loss for the year.

2. The Assessing Officer disallowed expenses on ground that expenses were neither found genuine nor any income had been offered against these expenses and added same to the assessee’s income and added said amount under the head ”profits and gains from business and profession” to the total income of the assessee.

3. On writ

Held:

1. In the facts of the instant case, it is undisputed that the addition of expenses made by the Assessing Officer in the impugned order was never ever claimed as a deduction by the assessee in its return of income. In other words, these expenses were never claimed as a deduction to give rise to the Assessing Officer to add back those deductions in the income returned by the assessee. The Assessing Officer wrongly relied on the accounting treatment to make the aforesaid addition. He failed to recall the well-established principle of law that treatment given by the assessee in its books of account is not decisive/conclusive for determining the taxable income under the Act. Whether an assessee is entitled to a deduction or not entirely depends upon the provisions of the Act de hors the disclosure in its books of account.

2. Therefore, the addition of expenses made by the Assessing Officer in the income returned by the assessee is wholly unsustainable.

3. As far as the request made for remanding the matter back to the Assessing Officer is concerned, there is no conceivable ground that has been brought on record based on which the request for remand has been made by the revenue. It is not as if the Assessing Officer was unaware

that no deduction has been claimed by the assessee. During the assessment proceedings, on more than half a dozen occasions, the assessee had highlighted this fact. Nevertheless, the Assessing Officer proceeded to make the aforesaid addition, and that too by relying upon the treatment given in the books of account of the assessee. Therefore, the addition made was a conscious act of the Assessing Officer and cannot be regarded as an error/oversight which would entail a remand. Accordingly, no purpose would be served if the matter is remanded to the Assessing Officer for a fresh consideration.

4. In view of the aforesaid discussion, the impugned assessment order passed for assessment year 2022-23, is hereby quashed and set aside along with the consequential demand notice and the penalty show cause notice.

Conclusion:

The Bombay High Court quashed the assessment order (and consequential demand and penalty notices) passed by the Assessment Unit/NFAC because the AO improperly made additions for expenses which the assessee had not claimed as deductions in its return of income. The Court held that the mere existence of expenses in the books of account does not entitle the AO to treat them as taxable income—especially when no claim was made by the assessee (or its unit holders) for those deductions. The Court reaffirmed the settled legal position that book entries are not conclusive for tax purposes, and the Assessing Officer’s action in adding back such unclaimed expenses was wholly unsustainable.

**************