You earn well. Maybe even very well. The salary hits your account every month, and for a moment just a moment everything feels fine.

Then somehow, by the 20th, the account looks thinner than it should. You can’t quite explain where it went. There was no big purchase, no emergency, no obvious mistake. Just a quiet, steady drain that you didn’t notice until it was too late.

If this sounds familiar, you are not alone. And more importantly you are not bad with money. You may just be missing a few things that nobody ever taught you.

This article is not about cutting your morning coffee or giving up things you enjoy. It’s about understanding why money slips through even capable, high-earning hands and what you can actually do about it.

First, Let’s Understand Why This Happens

The assumption most people make is: earn more, stress less. But income and financial clarity are not the same thing. Plenty of people earning 30,000 a month have more control over their finances than some earning 3 lakhs.

Here’s why high earners often still feel broke:

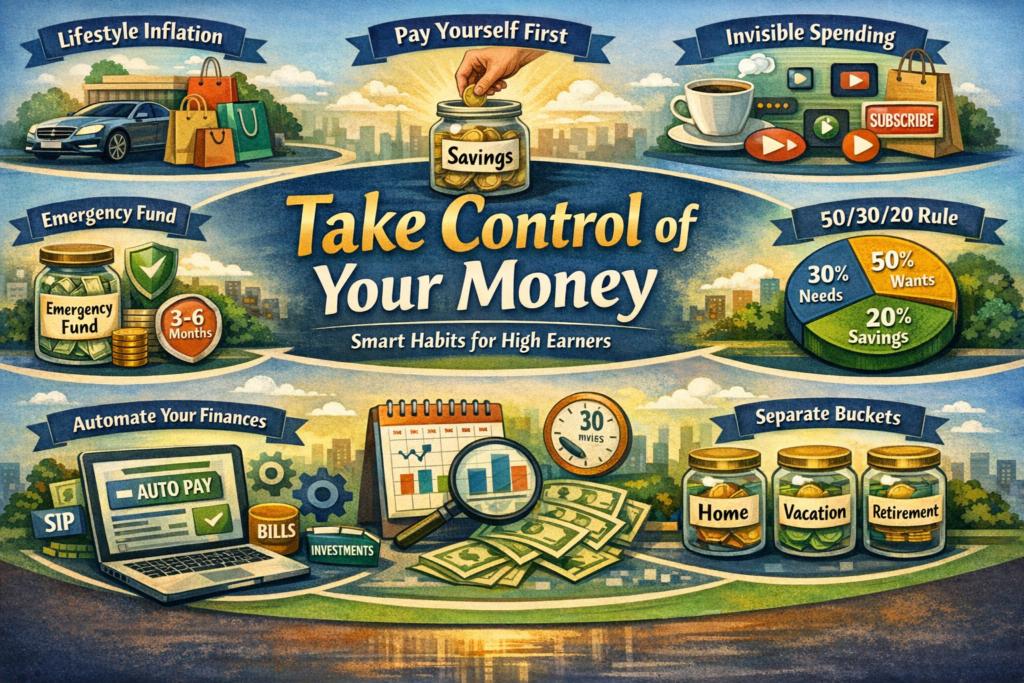

- Lifestyle inflation: Every time your salary increases, your expenses quietly rise to match it. A better phone, a bigger flat, more dining out. None of it feels extravagant in the moment. But together, it absorbs every increment you ever received.

- No system, just willpower: Most people try to control spending through discipline alone. But discipline is exhausting. Without a structure a real system you will always lose eventually.

- Invisible spending: Subscriptions, small UPI payments, impulse buys, the chai on the way to work. These feel too small to track. But over a month, they add up to thousands.

- Saving what’s left (instead of spending what’s left): If your approach is ‘I’ll save whatever remains at the end of the month,’ you will almost always save nothing. Because there will almost always be nothing left.

The problem is rarely how much you earn. It’s that no one ever showed you a that actually works for real life.

8 Practical Tips to Finally Take Control

These are not theories. They are habits and frameworks used by people who have turned their financial lives around people who earn exactly what you earn, have the same responsibilities, and live in the same world.

- Pay Yourself First Before Anyone Else

The moment your salary arrives, move a fixed amount to savings or investments immediately. Not at the end of the month. Not after bills. First. This one habit, more than anything else, separates people who build wealth from those who don’t. Even starting with some % of your income makes a real difference over time.

- Build a Simple Monthly Budget and Actually Use It

You don’t need a complicated spreadsheet. You need three categories: Fixed expenses (rent, EMIs, bills), Variable expenses (groceries, fuel, dining), and Savings/Investments. Assign a number to each. The act of writing it down even roughly changes how you spend. What gets measured gets managed.

- Use the 50/30/20 Rule as a Starting Point

50% of your income for needs. 30% for wants. 20% for savings and investments. This is not a rigid law it’s a framework. Adjust it to your life. But having any framework is infinitely better than having none.

- Do a Monthly ‘Money Date’ With Yourself

Set aside 30 minutes at the end of every month. Review what you spent. Compare it to what you planned. No judgment just awareness. Most people have never done this even once. Those who do it consistently are almost always in a better place financially within six months.

- Kill the Subscriptions You Forgot You Had

Open your bank statement right now and look at every auto-debit in the last 3 months. You will almost certainly find 2 or 3 subscriptions you forgot about or no longer use. Cancel them today. This is not about being frugal it’s about being intentional.

- Create Separate ‘Buckets’ for Different Goals

One bank account for everything is a recipe for confusion. Open a separate investment account or use help of Financial planning services advisor for each major goal like vacation, home down payment, whatever matters to you. When your money has a name and a purpose, it becomes much harder to spend mindlessly.

- Build an Emergency Fund Before Anything Else

Before investments, before that gadget, before anything else build a fund that covers 3 to 6 months of your expenses. Park it in a liquid mutual fund or a high-interest savings account. This is not about fear. It’s about freedom. When you have a buffer, you make better decisions everywhere in life.

- Automate Everything You Possibly Can

Set up automatic transfers to savings on salary day. Set up SIPs for investments. Set up auto-pay for bills. The more you remove money decisions from your daily willpower, the more consistent you’ll be. Good financial habits should require as little thinking as possible.

The Mindset Shift That Changes Everything

Managing money is not about restriction. It’s about intention.

There’s a big difference between spending because you chose to and spending because you weren’t paying attention. The first feels good. The second leaves you wondering where it all went.

Most salaried professionals were never taught personal finance in school. Nobody explained SIPs, emergency funds, or how lifestyle inflation quietly erodes income growth. You learned your job skills through years of effort. Financial clarity just needs the same attention and it rewards you far faster.

You don’t need to earn more to feel financially secure. You need a system that respects what you already earn.

Your 5-Minute Financial Health Check

Answer honestly. If you can say yes to most of these, you’re on the right track:

- Do you save or invest before spending each month?

- Do you have a rough budget, even a simple one?

- Do you have an emergency fund of at least 3 months’ expenses?

- Do you know roughly how much you spent last month?

- Are you working toward at least one clear financial goal?

If you answered no to three or more, that’s not a failure it’s a starting point. Pick one item from the list above and start there. Just one. This week.

A Final Thought

You worked hard to get to where you are. You deserve to feel the security that your income should be providing.

Financial stress is not a sign that you earn too little. It’s usually a sign that money hasn’t had clear direction. Give it direction. Build a simple system. Review it once a month. And be patient with yourself this is a skill, and like every skill, it gets easier with practice.

The goal isn’t to be perfect with money. The goal is to be conscious of it.

That shift from passive to intentional is where everything starts to change.

Your income is already enough. Now let’s make it work for you.