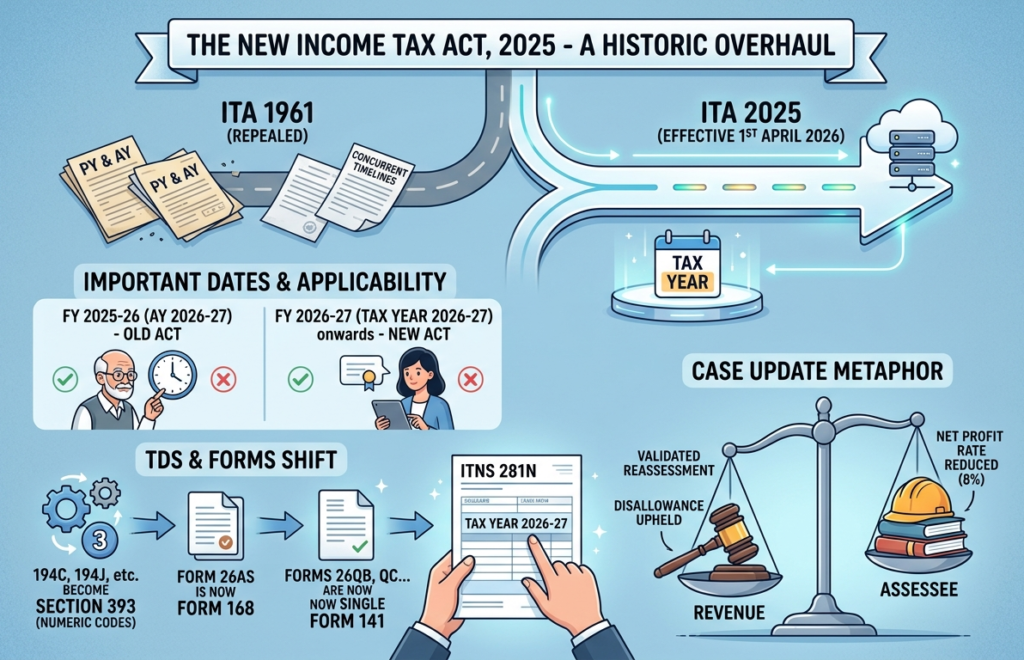

1. THE NEW INCOME TAX ACT, 2025 — A HISTORIC OVERHAUL

After 64 years, the Income Tax Act, 1961 stands repealed. The Income Tax Act, 2025 (ITA 2025) came into force on 1st April 2026, replacing every provision of the old Act with a cleaner, simplified framework. The Central Board of Direct Taxes (CBDT) also notified the Income Tax Rules, 2026 on 20th March 2026, along with redesigned forms, all effective from 1st April 2026.

The ‘Tax Year’ Concept — Biggest Terminology Shift

The old framework required understanding two concurrent timelines: Previous Year (when income is earned) and Assessment Year (when it is taxed, one year later). This was a source of perpetual confusion for clients.

The ITA 2025 replaces both terms with a single unified ‘Tax Year’, the financial year in which income is earned and reported. Tax Year 2026-27 covers 1st April 2026 to 31st March 2027.

| IMPORTANT: Applicability of Old vs. New Act |

| FY 2025-26 (AY 2026-27), Governed by the OLD Act (Income Tax Act, 1961) |

| FY 2026-27 (Tax Year 2026-27) onwards, Governed by the NEW Act (ITA 2025) |

| ITR for FY 2025-26 filed in 2026 will still use old section references. |

| The first return under ITA 2025 will be filed from July 2027 for Tax Year 2026-27. |

| All pending proceedings for years prior to 1 April 2026 continue under the old Act. |

No Change in Accounting Year

Since the Tax Year aligns with the Financial Year (April to March), no change in accounting year or financial statements is required for businesses. Your books of accounts structure remain exactly as before.

2. TDS for April 2026 — Your first payment under the new Income Tax Act, 2025

Due date: 7 May 2026 | Tax Year 2026-27 | New sections, new challan, new forms

The Income Tax Act, 1961 stands repealed from 1st April 2026. All TDS deductions for payments made on or after 1st April 2026 must be made under the Income Tax Act, 2025, using new section references and a new challan. Using old section numbers such as 194C, 194J, 194I, etc. for April 2026 transactions will result in system validation errors on the portal.

| Particulars | Details |

| Due date for April 2026 TDS | 7 May 2026 |

| Interest for late payment | 1.5% per month from date of deduction |

| Applicable Act | Income Tax Act, 2025 |

| Tax Year to be selected on challan | Tax Year 2026-27 (not Assessment Year) |

| New challan form | ITNS 281N |

Which Act Applies — The Golden Rule

- The Act that governs TDS depends on when the payment is made or when it is credited in the books, whichever is earlier.

- If that earlier event falls on or before 31 March 2026 — use the old Act (Income Tax Act, 1961).

- If that earlier event falls on or after 1 April 2026 — use the new Act (Income Tax Act, 2025).

- This applies even if the actual deposit to the government happens after 1 April 2026.

What Has Changed

What Has Changed

The familiar 194-series is completely replaced. All non-salary TDS is now governed by Section 393, which uses numeric payment codes 1001 to 1067. Salary TDS falls under Section 392. TCS falls under Section 394.

Assessment Year replaced by Tax Year

There is no longer an Assessment Year concept for new transactions. The challan now asks for Tax Year. April 2026 TDS must be filed under Tax Year 2026-27. Selecting the wrong year will cause reconciliation mismatches in Form 168 (the new equivalent of Form 26AS).

New forms replace old ones

- Form 26AS is replaced by Form 168.

- Form 16 (salary TDS certificate) is replaced by Form 130.

- Forms 26QB, 26QC, 26QD, and 26QE are all replaced by a single consolidated Form 141.

- Quarterly salary TDS return (Form 24Q) is replaced by Form 138.

Old Section vs. New Section — Quick Reference

| Nature of Payment | Old Section (1961 Act) | New Reference (2025 Act) | Rate |

| Salary | Section 192 | Section 392 | Slab rates |

| Contractor / works contract | Section 194C | Section 393 (Code 1003) | 1% / 2% |

| Professional / technical fees | Section 194J | Section 393 (Code 1008) | 2% / 10% |

| Rent — machinery / plant | Section 194I(a) | Section 393 (Code 1006) | 2% |

| Rent — land / building | Section 194I(b) | Section 393 (Code 1006) | 10% |

| Interest (bank) | Section 194A | Section 393 (Code 1001) | 10% |

| Commission / brokerage | Section 194H | Section 393 (Code 1005) | 2% |

| Dividend | Section 194 | Section 393 (Code 1002) | 10% |

| Purchase of immovable property | Section 194IA / Form 26QB | Section 393(1) / Form 141 Sch. A | 1% |

| Rent by individual / HUF | Section 194IB / Form 26QC | Section 393(1) / Form 141 Sch. B | 2% |

| Manpower supply | Section 194C or 194J (disputed) | Section 393 (Code 1003) — now explicitly ‘work’ | 1% / 2% |

How to Make the Payment — Step by Step

- Log in to the income tax portal (incometax.gov.in) using your TAN credentials.

- Go to e-Pay Tax and select Income Tax Act, 2025 (not 1961). For April 2026 TDS, this selection is mandatory.

- Select Tax Year 2026-27 (not Assessment Year). This is a new field — choosing the wrong option causes mismatches in Form 168.

- Select the relevant section: Section 392 for salary TDS, Section 393(1) / 393(2) / 393(3) for non-salary payments, or Section 394(1) for TCS. Enter the applicable payment code (1001 to 1067)

- Select the deductee type — Corporate or Non-Corporate — and enter the TDS breakup: Tax, Surcharge, and Education Cess separately. A separate challan is required for each deductee type and residential status.

- Select payment mode and complete payment using Challan ITNS 281N.

Special cases — Form 141: If you are deducting TDS on purchase of immovable property, rent payments (individual/HUF), payments to contractors/professionals by individuals, or Virtual Digital Assets — do not use the regular challan. Use Form 141, the new consolidated challan-cum-statement that replaces Forms 26QB, 26QC, 26QD, and 26QE. A separate Form 141 is required for each type of transaction.

3. Case Update: Ghanshyam Infrastructure (P.) Ltd. v. DCIT ITAT Ahmedabad Bench ‘A’

IT Appeal No. 1491 (Ahd.) of 2024 | AY 2010-11 | Decided: April 23, 2026

Background of the Case

Ghanshyam Infrastructure (P.) Ltd., a contractor, did not file its return of income for AY 2010-11. The Assessing Officer (AO), upon noticing contract receipts of ₹4.37 crores reflected in the assessee’s Form 26AS (with TDS duly deposited by the payer, Inter Globe Hotels Pvt. Ltd.), reopened the assessment under Section 147/148. The assessee cooperated minimally, and the AO conducted independent enquiries.

Key Issues & Rulings

1. Validity of Reassessment (In favour of Revenue)

The assessee challenged the reopening on two grounds — that the recorded reasons were vague/incorrect, and that the Section 148 notice was issued before obtaining sanction under Section 151. The Tribunal rejected both contentions. It held that at the time of recording reasons, the AO’s belief of escaped income was reasonable based on Form 26AS data and the non-filing of return. The fact that the invoice was dated in the preceding year came to light only during reassessment proceedings and could not invalidate the original reopening. On the sanction issue, the Tribunal found that the document cited by the assessee was merely a communication from the JCIT to the AO and did not establish that the Pr. CIT granted approval after the notice was issued.

2. Year of Taxability of Contract Income (In favour of Revenue)

The assessee argued the contract income pertained to AY 2009-10 (since the invoice was dated 31-03-2009) and was declared in AY 2010-11 only “to buy peace of mind.” The Tribunal disagreed, noting that TDS was deducted and paid in AY 2010-11, indicating the payer acknowledged the expense in that year. Crucially, the assessee failed to show the income was reflected in its books or return for the preceding year — in fact, the assessee itself offered the income in AY 2010-11. The Tribunal observed that a bill issued in one year but accepted by the other party in a subsequent year result in income accruing in the later year.

3. Net Profit Rate on Contract Receipts (In favour of Assessee)

The assessee offered profit at 8% on the contract receipts, but the AO estimated it at 12% without providing any specific justification for rejecting the 8% rate. The Tribunal found this unsustainable and directed the addition at 12% (amounting to ₹17.51 lakhs) to be deleted, accepting the assessee’s rate of 8%.

4. Disallowance of Finance Charges (In favour of Revenue)

The assessee claimed a loss of ₹17.59 lakhs comprising bank interest (₹16.37 lakhs) and bank charges (₹1.22 lakhs), which were reflected in the P&L account — a P&L that showed no contractual income at all. Since the assessee failed to establish any nexus between these expenses and its business, the disallowance was upheld.

Outcome: Appeal partly allowed. The addition on account of the higher profit rate (12%) was deleted; all other grounds were dismissed.